Wealth, at its core, is a language — and most people were never taught to speak it. For generations, the mechanics of compound interest, estate trusts, insurance ladders, and tax-advantaged accounts were passed down in boardrooms and country clubs, not kitchen tables. The gap between those who inherit financial fluency and those who have to self-educate their way into it has always been wide, sharp, and deliberately so. Vivian Tu, a former J.P. Morgan equities trader who made her first million by 27, built her entire platform — Your Rich BFF, a New York Times bestselling book franchise, and now over 10 million social media followers — on the premise that financial literacy is not a privilege. It is a right that was simply withheld.

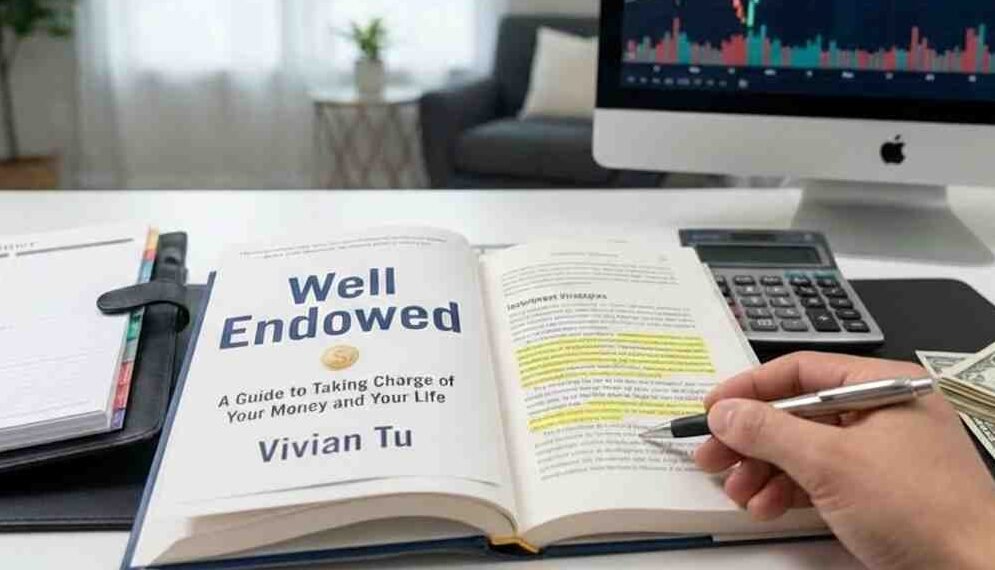

Her 2026 follow-up to Rich AF, aptly titled Well Endowed: The Secrets to Strategic Spending, Building a Financial Foundation for You and Your Family, and Creating Lasting Generational Wealth, picks up where the basics leave off. If Rich AF taught you to stop hemorrhaging money, Well Endowed teaches you what to build with what you’ve saved. It is a book written for the inflection point — that moment in your late twenties or thirties when the bills are paid, the emergency fund exists, and you’re staring at the question: Now what?

The answer, as Tu lays it out, is less about hustle and more about intention.

Spending Is a Strategy, Not a Weakness

One of the central reframes in Well Endowed is the rehabilitation of spending itself. The personal finance world has spent decades treating expenditure as the enemy — the vice to be controlled, the leak to be plugged. Tu rejects this moral architecture entirely. Every dollar spent, she argues, is a choice that shapes your future. The question is not whether to spend, but how to spend with precision.

This is a meaningful distinction. Strategic spending means directing capital toward assets that appreciate — real estate, education, experiences that compound — rather than consumption that evaporates. It also means aligning your spending with your stated values, which requires you to have stated values in the first place. Tu pushes readers to do that harder, more uncomfortable work of defining what actually matters before optimizing the ledger. A portfolio built without a philosophy is just noise.

The Rent-or-Buy Question, Finally Answered Honestly

Few financial debates generate more heat and less light than the homeownership question. Tu brings the nuance it deserves. Rather than defaulting to the inherited cultural wisdom that buying is always superior to renting, she walks through the actual calculus: local market conditions, your realistic timeline, the true cost of ownership (maintenance, taxes, opportunity cost of the down payment), and your personal liquidity needs.

For readers in high-cost markets — New York, California, the greater tri-state corridor — the math is not as obvious as it was for their parents’ generation. Tu breaks down the biggest financial decisions of your late twenties, thirties, and beyond, including homeownership, and teaches readers how to align their spending with their values and the legacy they hope to leave. Amazon That framing matters. A home purchased because “it’s what you do” is a different asset than a home purchased as a deliberate cornerstone of a multi-generational wealth strategy. The former may serve you. The latter almost certainly will.

Insurance Is Not Boring — It’s the Foundation

Nothing reveals financial immaturity faster than dismissing insurance. Tu devotes significant attention to the unsexy but load-bearing infrastructure of a sound financial life: life insurance, health coverage, disability, renters, even pet insurance gets a mention. The tendency among younger earners is to view insurance as money spent on nothing — a hedge against catastrophes that won’t happen to them.

Well Endowed dismantles that logic. Insurance is not a gamble against probability. It is the mechanism by which you protect the compounding momentum you’ve spent years building. A single catastrophic health event without proper coverage doesn’t just cost you money — it can collapse the entire architecture of a wealth-building plan. Tu’s Wall Street background shows here: she thinks in terms of downside protection, not just upside capture. Every serious portfolio manager knows that preserving capital is half the game.

Generational Wealth Without Creating Entitlement

Perhaps the book’s most philosophically rich terrain is Tu’s treatment of passing wealth to children. The paradox is real: you want to give your children the foundation you may not have had, but you don’t want to rob them of the hunger, the resilience, the street-level education that financial struggle often provides. Tu asks directly: how do you set your kids up with lasting generational wealth without making them lazy and entitled? Amazon

Her answer is not a formula but a philosophy. Generational wealth is transmitted most powerfully through financial literacy itself — through teaching children how money works, how to evaluate risk, how to delay gratification for compounding returns — not simply through the transfer of assets. A trust without an education to wield it is a liability. The goal is not to leave your children wealthy; it is to leave them capable.

Retirement Is Not a Number — It’s a System

The conventional retirement conversation revolves around a single, somewhat arbitrary number: How much do I need? Tu reorients the question toward systems and structures. How are your accounts organized? Are you maximizing tax-advantaged vehicles — 401(k), Roth IRA, HSA — in the right sequence for your income bracket? Are your investment allocations calibrated to your actual timeline rather than some generic age-based rule of thumb?

The book answers questions like how much to actually set aside for retirement, Amazon but more importantly, it explains why most people underprepare — not from laziness, but from a lack of framework. Tu provides that framework in plain language, grounded in the same equities-desk rigor she applied at J.P. Morgan, translated for readers who never sat on a trading floor.

Estate Planning Is Not for Old People

Wills. Trusts. Power of attorney. Healthcare directives. The vocabulary of estate planning carries the scent of old age and inevitability, which is precisely why people in their thirties avoid it. Tu treats this avoidance as one of the most expensive financial mistakes a young family can make.

Reviewers note that Tu thoughtfully tackles the topics that matter across a lifetime, including retirement and estate planning and even the ultimate end we all meet. Goodreads The argument is simple: the documents you need at fifty are exponentially easier and cheaper to establish at thirty-two. And without them, a lifetime of wealth-building can be significantly eroded — through probate costs, family disputes, or the blunt instrument of intestate succession laws that distribute assets according to the state’s preferences rather than your own.

Why This Book Matters Right Now

Financial stress in America is not an individual failure. It is a structural one — the product of a system that has historically kept the vocabulary of wealth inside certain ZIP codes and family trees. Vivian Tu’s contribution, across both her books and her broader platform, is the democratization of that vocabulary. Not through simplification, but through translation.

Well Endowed arrives at a moment when inflation, rising interest rates, and the psychological aftermath of pandemic-era economic whiplash have left a generation of earners genuinely uncertain about how to orient their financial lives. The book does not offer shortcuts. It offers something rarer and more durable: a clear-eyed framework for thinking about money not as a scoreboard, but as a tool — one that, when wielded with intention, can create stability, opportunity, and a legacy worth passing on.

The title is a double entendre worth taking seriously. To be well endowed is not to be born into wealth. It is to build a life so intentionally resourced that opportunity compounds on itself — for you, for your children, and for the community around you. That, as Tu argues and as the best financial minds have always known, is the actual game.

Well Endowed by Vivian Tu is available now at Amazon, Barnes & Noble, and independent booksellers nationwide. Follow Vivian Tu at yourrichbff.com and on her podcast Networth and Chill.