Everyone is crying over a seven percent mortgage. In 1981, the number was eighteen. You swallowed the blood, worked a second shift, and bought the house anyway — because the alternative was paying rent forever, and your father hadn’t come to this country so you could pay rent forever.

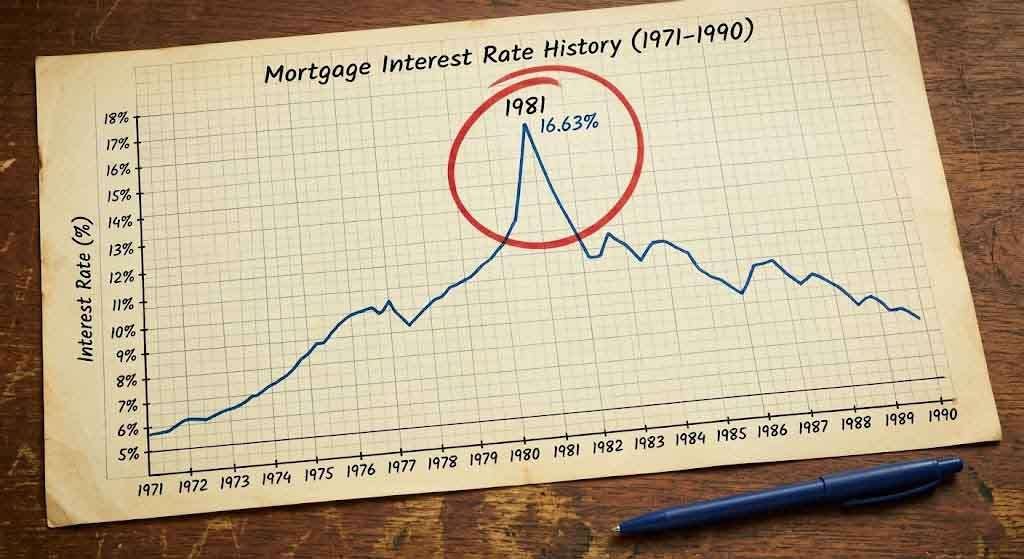

In October 1981, the average rate on a 30-year fixed-rate mortgage in the United States reached 18.63 percent. That figure comes directly from Freddie Mac’s Primary Mortgage Market Survey, which has tracked conventional mortgage rates since 1971. It is not a typo. It is not an outlier from a single lender. It is the average. It is what the market charged for the privilege of owning a home in Ronald Reagan’s America, while Paul Volcker at the Federal Reserve drove interest rates into the wall trying to kill the inflation that had been bleeding the economy for a decade.

People still bought houses.

How a Rate of 18 Percent Happens

Inflation in the United States through the 1970s was the product of multiple converging forces: the oil embargoes of 1973 and 1979, the fiscal pressures of Vietnam-era spending, the end of the Bretton Woods gold standard in 1971, and a Federal Reserve that had been too slow and too accommodating in its responses. By 1979, inflation was running above 13 percent annually. The dollar was losing value faster than working people could protect themselves from it.

Paul Volcker became Federal Reserve Chairman in August 1979 and made a decision that was economically sound and personally brutal: he would raise the federal funds rate until inflation broke. The federal funds rate — the rate at which banks lend to each other overnight, the rate that anchors borrowing costs across the economy — was pushed above 20 percent by mid-1981. Mortgage rates, which are tied to long-term expectations about inflation and the cost of money, followed.

The result was a recession. Unemployment climbed above ten percent. Construction collapsed. Auto sales collapsed. Farmers who had borrowed at floating rates to buy equipment and expand operations found themselves technically insolvent. Small businesses closed. The medicine was, by any measure, brutal.

And it worked. Inflation fell from over 13 percent in 1979 to under 4 percent by 1983. The Volcker disinflation is one of the few examples in monetary history of a central bank successfully breaking an entrenched inflationary spiral. It cost enormously. The people who paid the cost were not the architects of the policy.

What You Did If You Needed a House

If you were a working family in 1981 and you needed a house, you had limited options. You could wait — and wait, in the hope that rates would come down. Many people did. But waiting has costs too: rising rents, no equity accumulation, no stability for a family growing up in apartments. You could buy and absorb the rate. Or you could not buy at all.

The people who bought at eighteen percent did the math on what the payment meant and decided it was still worth it. On a $100,000 home with 20 percent down, at 18.63 percent over 30 years, the monthly principal and interest payment was approximately $1,185. That was a serious number for a family earning $25,000 or $30,000 a year. It was manageable — barely — if both spouses worked, if there were no surprises, if the car didn’t break down, if the kids didn’t get sick.

A lot of cars broke down. A lot of kids got sick. People managed anyway.

The houses they bought at 18 percent in 1981 were worth multiples of what they paid within twenty years. The families who absorbed that rate and held on came out ahead in ways they couldn’t have projected sitting at a kitchen table trying to figure out if they could make the number work.

Today’s Seven Percent in Context

The 30-year fixed mortgage rate in the United States has been hovering in the six-to-seven-and-a-half percent range through 2024 and into 2025. By historical standards, this is not an exceptional number. By the standards of the decade between 2010 and 2020, when rates spent extended periods below four percent and briefly touched three percent during the pandemic, it feels like a punishment.

The post-2020 rate environment spoiled a generation of buyers. Rates at three percent were not a natural condition. They were the product of Federal Reserve policy explicitly designed to stimulate an economy that had been hit by a once-in-a-century pandemic, layered on top of a decade of extraordinarily accommodative monetary policy following the 2008 financial crisis. Those rates were a gift. The gift has been revoked.

What’s happened to the Long Island market in this rate environment tracks the national pattern: reduced transaction volume, frustrated buyers who can’t reconcile what they expected to pay with what they’re actually being quoted, sellers reluctant to give up their three percent mortgages by listing and buying at six or seven. The market hasn’t collapsed. Prices on the North Shore have remained firm, supported by genuine scarcity and persistent demand from buyers relocating from the city.

The impact of interest rates on Long Island buyers right now is covered in detail on this blog — the short version is that rates are historically moderate, inventory is tight, and buyers who wait for three percent to return are going to wait a long time.

The Adjustable-Rate Gamble

One thing that kept transactions moving in the early 1980s was the adjustable-rate mortgage. ARMs, introduced in the late 1970s as a way to allow lenders to shift interest-rate risk onto borrowers, offered initial rates significantly below the fixed-rate market. If you believed rates would come down — and by 1982, there was evidence they were beginning to — an ARM was a calculated bet. You took the lower initial payment and planned to refinance when the market moved.

Many people were right. Rates fell steadily through the mid-1980s. The buyers who took ARMs in 1982 and 1983, then refinanced into fixed rates as conditions improved, ended up with manageable long-term payments and houses that had already appreciated significantly.

This is what the market rewards: not waiting for perfect conditions, but reading the trajectory well enough to act at the right moment. The people who waited for fixed rates to fall to comfortable levels before buying missed years of appreciation. The people who acted in imperfect conditions and adjusted their strategy as conditions changed came out ahead.

What Pawli Sees in Today’s Market

Pawli at Maison Pawli works with buyers across the North Shore who are making this calculation right now: is this the moment to act, or is this the moment to wait? Her perspective, grounded in the current inventory data and the specific dynamics of the Mount Sinai and Miller Place markets, is consistent with what the historical record suggests — that waiting for ideal conditions is itself a choice with costs, and that those costs compound over time.

The families who bought on Long Island in 1981, when the rate was 18.63 percent and the payment was brutal and nobody knew how long the pain would last — those families have equity today that represents decades of wealth accumulation. The rate they paid at origination is a footnote.

The rate is never the whole story. It’s one variable in a calculation that includes appreciation, rental costs forgone, tax benefits, and the compounding value of owning your own place. In 1981, people understood that because they had no choice but to understand it. The rate was terrifying and they signed the paper anyway.

There’s a lesson in that for anyone sitting at a kitchen table today, staring at a seven percent quote, wondering whether the number is too high to move.

It is not 1981. It is not eighteen percent. Sign the paper.

You Might Also Like

- The Impact of Interest Rates on Long Island Buyers Right Now

- First-Time Homebuyer’s Roadmap for Long Island in 2026

- Long Island Real Estate Market Update: Q1 2026

Sources

- Freddie Mac Primary Mortgage Market Survey (PMMS) — Historical Data. freddiemac.com/pmms/archive

- Federal Reserve History — The Great Inflation. federalreservehistory.org

- Federal Reserve Bank of St. Louis (FRED) — 30-Year Fixed Rate Mortgage Average. fred.stlouisfed.org

- Meltzer, Allan H. A History of the Federal Reserve, Volume 2. University of Chicago Press, 2009. amazon.com